THANK YOU FOR SUBSCRIBING

Capitalmarkets CIO Outlook Weekly Brief

Be first to read the latest tech news, Industry Leader's Insights, and CIO interviews of medium and large enterprises exclusively from Capitalmarkets CIO Outlook

Ryan Nauman, Market Strategist, Informa Financial Intelligence.

Ryan Nauman, Market Strategist, Informa Financial Intelligence.Over 30 years have passed since William Sharpe introduced returns-based style analysis (RBSA) to the investment world in his landmark article, “Determining a Funds Effective Asset Mix.”In 1992, RBSA became commercially available through Zephyr Style ADVISOR. Numerous other software programs have followed suite by offering RBSA within their applications.

Style analysis dates back to the ’70s when institutional consultants detected different patterns of returns for managers who employed different investment processes. This difference in return behavior led to the term “style.” Consultants then started to label managers according to style.

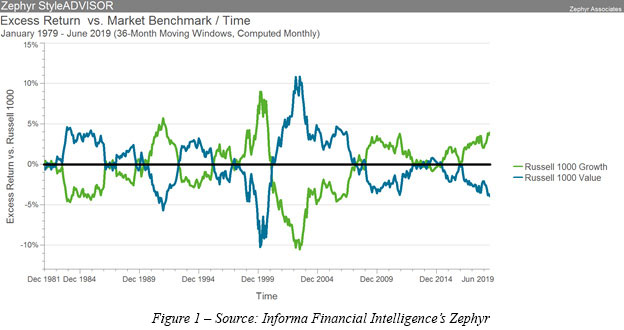

During this time, it became clear that the return behavior of these unique styles was cyclical. There were periods of time when value stocks outperformed growth stocks and vice versa. A manager’s skill did not determine these cycles, as they were simply a function of the market, or systematic risk factors. Figure 1 displays this style behavior, as we examine the excess returns of the Russell 1000 Growth (blue line) and Russell 1000 Value (red line) indexes over the Russell 1000 index (black horizontal line at 0%.).This example shows the importance of recognizing a manager’s style to identify an appropriate benchmark and building a diversified portfolio.

Rather than determining the manager’s style by looking at the actual holdings, RBSA identifies the style by looking at the manager’s behavior. Sharpe recognized that by using a manager’s historical returns, along with the returns of selected indexes, one could determine the combination of indexes that is most highly correlated with the manager’s returns. Sharpe referred to a manager’s return behavior as his “tracks in the sand.”

Rather than determining the manager’s style by looking at the actual holdings, RBSA identifies the style by looking at the manager’s behavior. Sharpe recognized that by using a manager’s historical returns, along with the returns of selected indexes, one could determine the combination of indexes that is most highly correlated with the manager’s returns. Sharpe referred to a manager’s return behavior as his “tracks in the sand.”

RBSA allows you to forecast the manager’s asset class exposure, and therefore how the manager returns will behave relative to the indexes. One can see how this information can be very useful when creating a diversified portfolio.

Knowing that 95% of a portfolio’s return variations are attributed to asset allocation, constructing your asset allocation and selecting managers that behave similar to the corresponding asset classes is crucial to your overall performance.

After determining optimal asset allocation, one must select managers that fill the specific roles within the portfolio. Identifying how a manager behaves during certain market cycles ensures that you will have the proper managers in place to complete an effective asset mix for your clients. Much like a sports team, each individual manager has a specific job to do in order for that portfolio to accomplish its goals. Using RBSA helps determine the best fit position for a manager, resulting in an optimal effective portfolio mix for your client.

Determining the fund’s exposure to the different asset classes will help provide the knowledge one needs to improve portfolio diversification. Relying too heavily on the fund objective or stated category may lead to unintended performance and/or behavior, which could reduce portfolio diversification. Alternatively, one should look at how the returns of the fund behaves. Ideally, you would like one fund that zigs while the other zags, like Figure 1.

Read Also